Many lenders appear to be significantly underestimating the burgeoning opportunity presented by embedded lending, potentially ceding market share and bottom-line growth.

According to a recent report, “Embedded Lending: From the Lender’s Perspective,” commissioned by Visa and produced by PYMNTS, embedded lending involves integrating credit tools directly into a merchant or provider’s platform, allowing borrowers to apply for credit at the point of payment for a product or service. This differs from traditional lending, where consumers use existing credit cards or personal loans. While embedded lending is becoming a prominent feature in both consumer and SMB segments across six major economies surveyed — Australia, Germany, India, Japan, the United Kingdom and the United States — a sizable share of lenders, particularly those serving SMBs, have not fully embraced its potential. Roughly 45% of lenders serving SMBs currently do not offer any embedded lending product. Even among those offering embedded options, interest in launching new embedded lending products in the next two years is notably low, with only about 1 in 5 lender respondents indicating they are very or extremely interested.

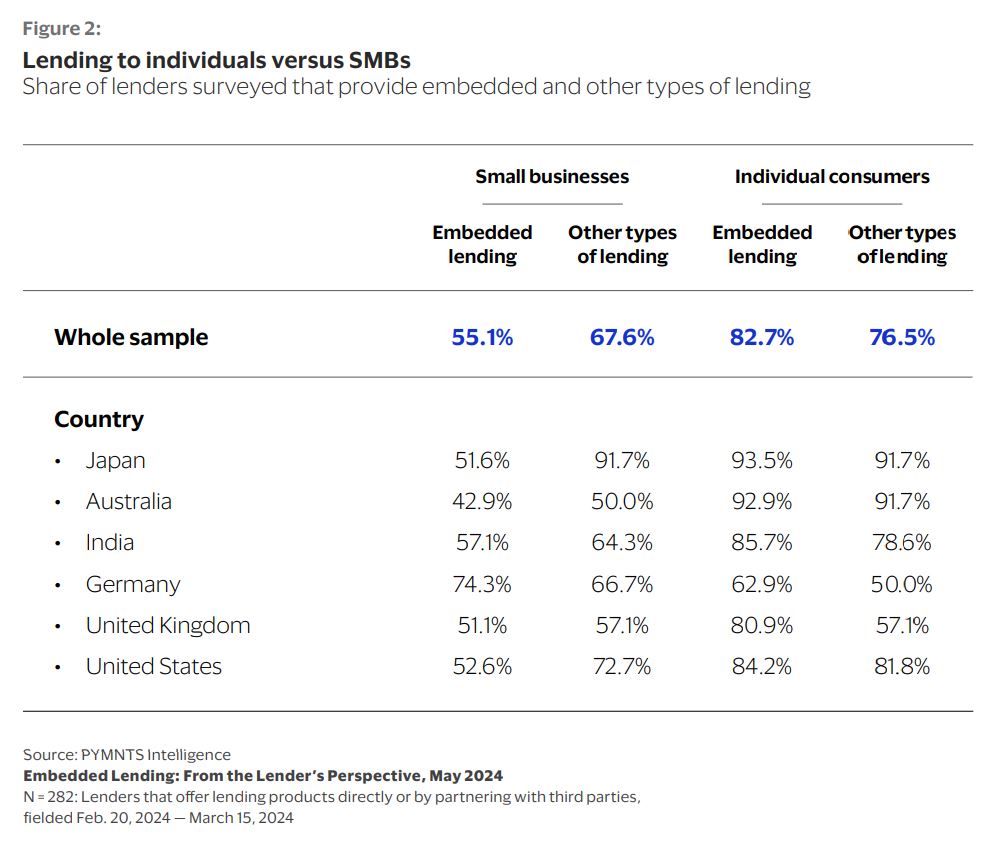

The report, based on a survey of 361 lenders conducted from Feb. 20 to March 15, 2024, highlights that lenders offering embedded solutions are largely overlooking the SMB segment by focusing primarily on consumers. For example, 83% of lenders offer embedded lending products to customers, compared to 55% that serve SMBs. Furthermore, lenders are widely underutilizing external platform integrations, such as with eCommerce platforms or in-store point-of-sale systems, which are crucial for reaching new customers and facilitating embedded experiences directly within the transaction flow.

Only 58% of lenders serving consumers have at least one third-party platform integration, and this figure is just 64% for those serving SMBs. This underutilization persists even among integrated lenders; only 37% of consumer lenders, for instance, have integrated with eCommerce platforms. This contrasts sharply with substantial consumer and SMB demand, as 43% of consumers and 37% of SMBs surveyed are very or extremely interested in switching to a provider that offers embedded lending. Lenders with increased net profits in 2023 were found to be more interested in new embedded lending products and more likely to have embedded lending in their portfolios.

Key data points from the report include:

- Nearly half (45%) of lenders serving SMBs do not currently offer any embedded lending product.

- Only 22% of lenders lending to consumers and 22% of lenders lending to SMBs express very or extremely high interest in offering new embedded lending products in the next two years.

- A significant share of consumers (43%) and SMBs (37%) are very or extremely interested in switching to a provider that offers embedded lending options.

The report also delves into the obstacles deterring lenders from entering the embedded lending space, citing technology integration and infrastructure challenges (34%), operational and scalability issues (23%), and risk management and credit assessment (22%) as the biggest concerns for those not currently offering such products. It notes varying challenges across different countries.

The report also identifies specific embedded lending products lenders are most interested in offering in the future, including embedded personal loans (67% of consumer lenders not currently offering) and embedded microloans or microfinance products (67% of SMB lenders not currently offering). The data underscores a significant opportunity for lenders to better align their embedded lending strategies with market demand and leverage external integrations more effectively.

The post Nearly Half of SMB Lenders Overlook Embedded Opportunity, Study Finds appeared first on PYMNTS.com.